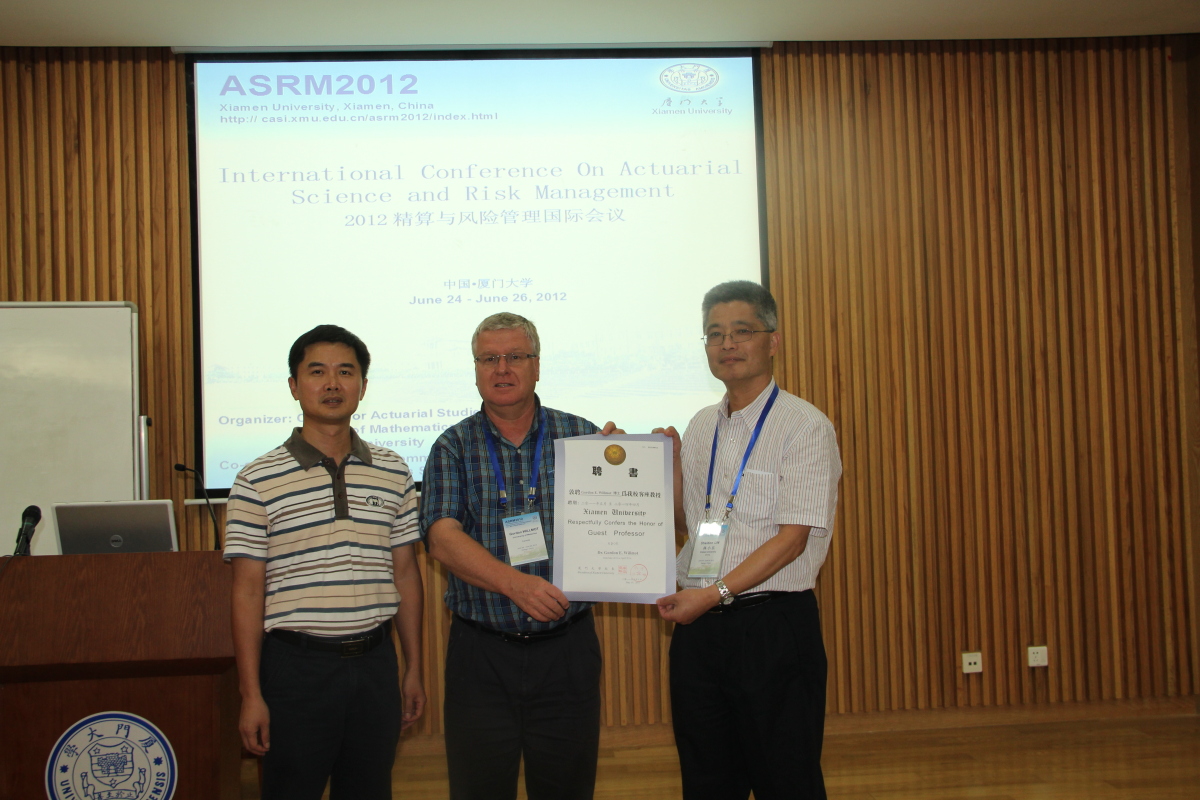

6月24-27日,加拿大滑铁卢大学的Gordon Willmot教授、南开大学数学学院郭军义教授应邀到我校参加2012精算与风险管理国际会议,并欣然接受学校的聘请,受聘厦门大学精算中心兼职教授。26日下午,在厦门大学科学艺术中心1号报告厅,厦门大学精算中心主任向Gordon Willmot教授和郭军义教授颁发了厦门大学兼职教授聘书。学院党委张明智书记参加了聘书颁发仪式,感谢Gordon Willmot教授、郭军义教授对我校精算专业建设的大力支持。他们的加盟,必将强有力地促进学院的统计和精算研究、学生培养和对外交流等方面建设。

近年来,学院重视加强厦门大学精算中心建设,在中心主任的努力下,对中心未来的目标作了详细规划,不断加强师资队伍建设,通过引进来、送出去培养等方式提升队伍水平。召开国际会议,邀请国内外知名精算专家莅临会议,营造良好的学术氛围,扩大我校精算专业的影响。搭建交流平台,让青年教师有更多的机会与知名专家学者交流学习的机会。目前,精算中心各项工作正有条不紊的开展中。

人物名片:

1.Gordon Willmot教授

现就职于加拿大滑铁卢大学,是国际知名的精算学专家。在多个学术团体任职:Fellow of Society of Actuaries (FSA) and Fellow of Canadian Institute of Actuaries (FCIA) since 1989

1996-1998 Society of Actuaries Working Group on Courses 3 and 4

1994-1999 Society of Actuaries - Co-chairperson of Course 152 - Intensive Seminar on Risk Theory

1995-1998 Society of Actuaries-Education and Research Section Council

Refereeing-various probability, statistics, operations research, and actuarial journals

Editorial Duties

(a) Associate Editor of Insurance: Mathematics and Economics(2010-).

(b) 2004 Section Editor (Claims Distributions) for the Encyclopedia of Actuarial Science, John Wiley, Chichester.

(c) Associate Editor of the Australian & New Zealand Journal of Statistics (2002-).

(d) Associate Editor of the North American Actuarial Journal (1997-2003).

(e) Guest Editor of a special issue of Insurance: Mathematics and Economics devoted to refereed proceedings of the 23rd Actuarial Research Conference held at the University of Waterloo, Waterloo, Ontario, June29-30, 2006.

Scientific Committee 。

主要学术成果有:

[1] Cheung, E.C.K., Landriault, D., Willmot, G.E., and Woo, J.K. On orderings and bounds in a generalized Sparre Andersen risk model, Applied Stochastic Models in Business and Industry, 2011, to appear.

[2] Willmot, G.E., and Lin, X.S. Risk modelling with the mixed Erlang distribution, Applied Stochastic Models in Business and Industry, 2011, to appear.

[3] Kim, S.Y., and Willmot, G.E. The proper distribution of the deficit in the delayed renewal risk model. Scandinavian Actuarial Journal, 2011, to appear.

[4] Willmot, G.E. Distributional analysis of a generalization of the Polya process, Insurance: Mathematics and Economics, 2010, 47, 423-427.

[5] Willmot, G.E., and Woo, J.K. Surplus analysis for a class of Coxian interclaim time distributions with applications to mixed Erlang claim amounts. Insurance: Mathematics and Economics, 2010, 46, 32-41.

[6] Cheung, E.C.K., Landriault, D., Willmot, G.E., and Woo, J.K. Structural properties of Gerber-Shiu functions in dependent Sparre Andersen models. Insurance: Mathematics and Economics, 2010, 46, 117-126.

[7] Cheung, E.C.K., Landriault, D., Willmot, G.E., and Woo, J.K. Gerber-Shiu analysis with a generalized penalty function. Scandinavian Actuarial Journal, 2010, 185-199.

[8] Willmot, G.E., and Drekic, S. Time-dependent analysis of some infinite server queues with bulk Poisson arrivals. INFOR, 2010, 47, 297-303.

[9] Cai, J. Feng, R., and Willmot, G.E. On the total discounted operating costs up to a default and its applications. Advances in Applied Probability, 2009, 41, 495-522.

[10] Cai, J., Feng, R. and Willmot, G.E. Analysis of the Compound Poisson Surplus Model with Liquid Reserves, Interest and Dividends. Astin Bulletin, 2009, 39, 225-247.

[11] Cai, J., Feng, R., and Willmot, G.E. The compound Poisson surplus model with interest and liquid reserves: Analysis of the Gerber-Shiu discounted penalty function. Methodology and Computing in Applied Probability, 2009, 11, 401-423.

[12] Landriault, D., and Willmot, G.E. On the joint distributions of the time to ruin, the surplus prior to ruin, and the deficit at ruin in the classical risk model. North American Actuarial Journal, 2009, 13, 2, 252-270. Discussion, 2009, 13, 2, 271-278. Authors' reply, 2009, 13, 2, 278-279.

[13] Landriault, D., and Willmot, G.E. On the Gerber-Shiu discounted penalty function in the Sparre Anderson model with an arbitrary interclaim time distribution. Insurance: Mathematics and Economics, 2008, 42, 600-608.

[14] Willmot, G.E., and Woo, J.K. On the class of Erlang mixtures with risk theoretic applications. North American Actuarial Journal, 2007, 11, 2, 99-115. Discussion, 2007, 11, 2, 115-117. Authors' reply, 2007, 11, 2, 117-118.

[15] Willmot, G.E. On the discounted penalty function in the renewal risk model with general interclaim times. Insurance: Mathematics and Economics, 2007, 41, 17-31.

[16] Pavlova, K.P., Cai, J., and Willmot, G.E. The preservation of classes of discrete distributions underconvolution and mixing. Insurance: Mathematics and Economics, 2006, 38, 391-405.

[17] Cai, J., and Willmot, G.E. Monotonicity and Aging Properties of Random Sums. Statistics and Probability Letters, 2005, 73, 381-392.

[18] Dickson, D.C.M., and Willmot, G.E. The density of the time to ruin in the classical Poisson risk model. Astin Bulletin, 2005, 35, 45-60.

[19]Drekic, S., and Willmot, G.E. On the moments of the time of ruin with applications to phase-type claims. North American Actuarial Journal, 2005, 9, 2, 17-30.

[20] Willmot, G.E., Drekic, S., and Cai, J. Equilibrium compound distributions and stop-loss moments. Scandinavian Actuarial Journal, 2005, 6-24.

2.郭军义教授

现就职于南开大学数学学院,是国内概率统计研究领域中的知名学者,已经公开发表学术论文几十篇,其中大部分论文发表在国际统计和保险精算的主流期刊上。是天津数学会副理事长、概率统计学会常务理事、中国数学、力学物理学与高新技术交叉研究学会常务理事、“Interdisciplinary Sciences”编委、《应用概率统计》编委、IMS-China成员。

主要学术成果有:

1. Guo, Jun Yi; Yang, Xiang Qun Three-point transition functions for two-parameter Markov chains and their four systems of partial differential equations. Sci. China Ser. A 35 (1992), no. 7, 806–818

2. Junyi Guo. Stopping lines and their relations. Chinese Journal of Applied Probability and Statistics, 13, 171-174,1997

3. Junyi Guo, Rong Wu. Super-Brownian motion on the Sierpinski gasket with point catalytic medium, In: Trends in Probability and Related Analysis,(editors N. Kono & N. R. Shieh) World Scientific. 1997. 159-166. Proceedings of SAP'96 1997

4. Junyi Guo. Path properties of super-Brownian motion with a more general branching mechanism. Chinese Annals of mathematics,18, 673-686, 1997

5. Junyi Guo. Some path properties of Brownian motion and super-Brownian motion on the Sierpinski gasket. Acta Mathematica Scientia, 17,143-150, 1997

6. Junyi Guo. Local extinction of super-Brownian motion on the Sierpinski gasket. Science in China , 41, 260-266, 1998

7. Junyi Guo, Rong Wu. The behavior of Super-Brownian motion near extinction. Acta Mathematica Sinica(New Series), 14,315-320, 1998

8. Junyi Guo. The limitting behaviour of super-Brownian motion on Sierpinski gasket, Chinese Science Bulletin, 43(7),614-614,1998

9. Junyi Guo. Oscillation of occupation time processes of super-Brownian motion on the Sierpinski gasket. Science in China,43(12), 1250-1257, 2000

10. Junyi Guo. A class of super diffusions on Sierpinski gasket. Chinese Annals of Mathematics. 21(6)A, 763-770, 2000

11. Kam C. Yuen, Junyi Guo. Ruin probabilities for time-correlated claims in the compound binomial model. Insurance:Mathematics and Economics, Vol: 29 No.1 47-57 ,2001

12. Yuen, KC; Guo, JY; Wu, XY. On a correlated aggregate claims model with Poisson and Erlang risk processes. INSURANCE MATHEMATICS & ECONOMICS Vol. 31 No. 2 ,205-214 ,2002

13. Yuen, Kam C.; Guo, Junyi; Ng, Kai W. On ultimate ruin in a delayed-claims risk model. J. Appl. Probab. 42 (2005), no. 1, 163–174.

14. Yuen, Kam C.; Guo, Junyi; Wu, Xueyuan On the first time of ruin in the bivariate compound Poisson model. Insurance Math. Econom. 38 (2006), no. 2, 298–308.

15. Zhou, Ming; Wei, Li; Guo, Jun-yi Some results behind dividend problems. Acta Math. Appl. Sin. Engl. Ser. 22 (2006), no. 4, 681–686

16. Yuen, Kam-Chuen; Guo, Junyi Some results on the compound Markov binomial model. Scand. Actuar. J. 2006, no. 3, 129–140.

17. Zhang, H. Y.; Zhou, M.; Guo, J. Y. The Gerber-Shiu discounted penalty function for classical risk model with a two-step premium rate. Statist. Probab. Lett. 76 (2006), no. 12, 1211–1218

18. Liu, S. X.; Guo, J. Y. Discrete risk model revisited. Methodol. Comput. Appl. Probab. 8 (2006), no. 2, 303–313.

19. Liang, Zhibin; Guo, Junyi Optimal proportional reinsurance and ruin probability. Stoch. Models 23 (2007), no. 2, 333–350.

20. Xiao, Yuntao; Guo, Junyi The compound binomial risk model with time-correlated claims. Insurance Math. Econom. 41 (2007), no. 1, 124–133.

21. Zhang, Xin; Zhou, Ming; Guo, Junyi Optimal combinational quota-share and excess-of-loss reinsurance policies in a dynamic setting. Appl. Stoch. Models Bus. Ind. 23 (2007), no. 1, 63–71

22. Guo, Jun Yi; Yuen, Kam C.; Zhou, Ming Ruin probabilities in Cox risk models with two dependent classes of business. Acta Math. Sin. (Engl. Ser.) 23 (2007), no. 7, 1281–1288.

23. Bai, Lihua; Guo, Junyi Utility maximization with partial information: Hamilton-Jacobi-Bellman equation approach. Front. Math. China 2 (2007), no. 4, 527–537

24. Liang, Zhibin; Guo, Junyi Upper bound for ruin probabilities under optimal investment and proportional reinsurance. Appl. Stoch. Models Bus. Ind. 24 (2008), no. 2, 109–128.

Zhou, Ming; Guo, Junyi Classical risk model with threshold dividend strategy. Acta Math. Sci. Ser. B Engl. Ed. 28 (2008), no. 2, 355–362.